In the second quarter of 2019, Indian mobile payment leader PayTM surpassed China in the number of deals. Such a feat has been achieved while India is still an evolving fintech market in comparison to the developed fintech market like China. Red-tapism and the immense number of laws are the reasons of slow down for the FinTech market in India, but strict regulations are inevitable when it comes to a financial or technological company. The Steering Committee on FinTech related issues constituted by the Ministry of Finance, Department of Economic Affairs, submitted in September 2019 its report indicating various trends and challenges related to FinTech in India. This post discusses the same in brief. This post is the second one in the series of ‘Simplifying FinTech and FinTech Laws’.

Trends related to Fintech in India

The FinTech sector in India is thriving and growing expansively, enabled by a large consumer base, innovatively boosted startups and balanced regulatory policies in the form of ‘Digital India’ programme. The Indian Fintech industry has grown by 282% in the last decade and has reached the valuation of USD 450 million in 2015. Currently, there are more than 400 fintech companies that are working in India and the investments are to be fueled with 170% by 2020. The Indian fintech market is expected to grow by USD 2.4 million by 2020 from the present USD 1.2 billion, as per NASSCOM report. The transactional value of Indian fintech sector is evaluated to be USD 33 billion in approx in 2016 and is further forecasted to reach the point of USD 73 billion by 2020.

FinTech facilities in India

The primary facilities offered by companies operating in the space of fintech are:

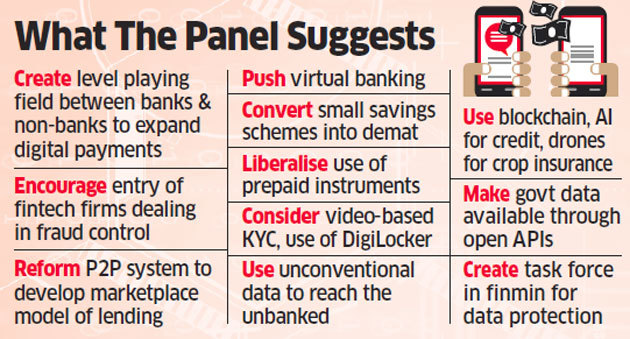

Pre-paid Payment Instruments

Also known as PPIs, this instrument enables the user to engage in the purchase of products that include products relating to financial services as well. To be able to purchase the products, a value entered into the e-wallets in the PPIs so as to make purchases against that value. There are 3 types of PPIs: Closed, semi-closed and open systems. Depending on the type, one may also have the facility to withdraw cash from the PPIs. Other than the banks, they can only be issued by institutions authorized to function in the arena of e-wallets or pre-paid card services.

UPI Payments

Managed by the National Payments Corporation of India, the UPI (Unified Payment Interface) provides a platform for quicker real time-based transactions, facilitating ease for the smartphone users to enter into multiple transactions with a lower cost than what the traditional method demands. Constituting a major part of the consumer behaviour in the market, the UPIs enable universality to the transactions they wish to enter in and engage in the greater number with the traders.

Digital Transactions

In the traditional financial market, it was only the banks that could lend money. However, with the convergence of technology and financial market, loans nowadays are even dispersed by non-banking financial companies, also known as NBFCs. The NBFCs with their interactive and user-friendly applications have attracted wide userbase in the digital arena to enter into credit purchasing, loan system after verification.

Lending Platforms

These lending platforms offered are Peer to Peer based. Such platforms bring together willing lenders and borrowers to enter into regulated transactions. As per the guidelines issued by RBI in this regard, the lending platforms can only be offered by the registered non- banking companies in India.

Online Sale and Purchase

The recent trends amongst many have also been that of online sale and purchase. To facilitate the same there requires to be a system whereby an entity collects payments form the purchases and send it across to the sellers. The entities involved in this function are known as payment aggregators or intermediaries. These entities electronically consolidate the payments done and transfer the same to the sellers.

Banking Services

Once begun as a measure to penetrate into the grassroots level of society the banking system and provide ease to the customers, digital banking services by the payment banks have now become a feature of the payment banks. The RBI has allowed payment banks to offer basic services involved in smooth banking by the customers online. This includes facilities such as accepting deposits (though RBI has placed a limit on it), view transactions, transfer funds, etc. However, this arena remains strictly regulated for not all facilities remain digitally available such as issuing credit cards.

Regulatory Challenges to Fin-Tech in India

While in India, digital finance firms are thriving as the government is continuing to issue pro-startup regulations and policies, the central regulatory body for Fintech i.e. the Reserve Bank of India, still suffers due to a traditionally rooted and established infrastructure which cannot be easily replaced with the updated regulatory framework that matches the advancements of technology.

Indian market is already recognized as the conservative and restrictive market and henceforth makes it difficult for Fintech firms to further instil the confidence in adopting the Fintech services in the absence of any concrete regulatory framework.

The commendable steps have been taken by the Indian government and regulatory institutions in a prompt manner, however, policies and regulations have to match the pace with which technological advancements in the finance sector taking place. This is much needed to ensure secure a transparent growth of Fintech in India.

Regulatory Uncertainty in the Fintech Sector

The foremost challenge that the regulator for the fintech sector has to dealt with by it the lack of regulations. Moreover, if there are regulations then to consolidate them is another major challenge. There is a requirement to “to support the formulation of policies that foster the benefits of fintech and mitigate potential risks”. Henceforth, a regulator or policy-maker has to work in the directions of “the modification and adaptation of regulatory frameworks to contain risks of arbitrage, while recognizing that regulation should remain proportionate to the risks.”

Digital On-boarding and Financial Inclusion

The two significant challenges that one can see as the huge mountainous tasks in the Indian context are: firstly, making the fintech platforms accessible to every Indian and secondly, analyzing the risks that are potentially present in trying out a scheme to provide digital onboarding. The Supreme Court recently decided upon the constitutionality of the Aadhaar, the ambitious government project to provide a unified identity. Aadhaar has been held constitutional but Section 57 of the Aadhaar Act was struck off. Section 57 provided the mandatory verification and linking procedure for consumers to avail a company’s service. The judgment is having serious implications on the government’s efforts to provide frictionless onboarding of consumers.

“The judgement impacted the delivery of financial services across verticals including bank account opening, loans, mutual funds and insurance. Though the judgement allows voluntary use of Aadhaar by consumers, there are multiple interpretations of it and the Unique Identification Authority of India (UIDAI) has resorted to safer approaches to avoid any more legal battles and stopped services to private entities altogether.”

Low Credit for Startups

Investors in the market are now hesitant to invest in fintech startups. The investors are baulking as there have been quite a number of bad loan incidents. The big setback to the fintech industry as well as the financial sector came into the form of IL&FS breakdown. The company defaulted against the inter-corporate deposits and commercial papers or borrowings. The incident has affected the whole fintech industry as the crisis included lending businesses that were key to a number of NBFCs as a funding source.

e-NACH crisis

The Apex Court’s judgment brought down to stoppage, another popular mode of financing which is also the foremost mode of debit for lenders, MFs and insurance, as in pulling money from customer’s account. This is yet another judgment that has slowed down the advancement and has promoted the traditional manner of physical registrations.

Data Protection

Both the traditional banking system and the fintech services gather a large number of data records from various of their clients, which contains a profile of behavioural and financial information. Though the utility of such data is positive when it is used for a specific purpose of improving the services, it leads to giving way to a heap of privacy issues as well, especially when the financial service provider engages a third party’s technology services.

The judiciary recognized the risk of data privacy to the banking sector’s consumer in the case of Punjab National Bank v Rupa Mahajan Pahwa, “in which Punjab National Bank had issued a duplicate passbook of a joint savings bank account, held between the petitioner and her husband, to an unauthorized person”.

Other Challenges to the Fintech system in India

In terms of regulatory standards, India lacks in providing a comprehensive cybersecurity framework to reduce the cyber-crime issues. The competition law has also, in some sort of stages, have failed to control the domination of certain advance fintech NBFCs.

Recommended Readings:

- Fintech in India: Powering Digital Economy, NASSCOM, at https://community.nasscom.in/download.php?file=wp-content/uploads/attachment/18283-fintech-lending—unlocking-untapped-potential.pdf.

- Opinion: The Challenges for fintech adoption in India, LiveMint, at https://www.livemint.com/Opinion/Wyt5KOOS43ebC4feFCiYWN/The-challenges-for-fintech-adoption-in-India.html.

- Justice (retd.) KS Puttasamy v. Union of India, 2017 10 S.C.C. 1.

- Jitendra Gupta, 3 major setbacks for fintech industry, LiveMint, at https://www.livemint.com/Money/jxepdJVODLb6fGDfhue6qI/3-major-setbacks-for-fintech-industry.html.

- Punjab National Bank v Rupa Mahajan Pahwa, IV (2015) CPJ 620 (NC).